Looking for clear answers to common health insurance questions in Texas?If this topic has raised questions in your mind, that is completely normal. Many Texans want to understand costs, coverage, doctor networks, and enrollment before choosing a plan.

That is why this guide answers the most common questions people have before choosing coverage. At Wilkerson Insurance Agency, we have been helping individuals, families, retirees, and small business owners across Texas since 2010. As an independent agency based in Farmers Branch, TX, we are not tied to just one insurance company.That means we can compare options from multiple carriers and help you understand what fits your needs, budget, and situation more clearly. Our team focuses on personal guidance, honest comparisons, and year-round support.

In this blog, you will learn:

- how health insurance plans work in Texas

- the difference between premiums, deductibles, copays, and coinsurance

- whether you may qualify for subsidies or premium tax credits

- when you can enrol or change your health insurance

- how pre-existing conditions are covered

- the difference between HMO and PPO plans

- the biggest mistakes Texans make when choosing coverage

- how a local Texas health insurance broker can help you compare plans more confidently

How Do Health Insurance Plans Actually Work in Texas?

Health insurance works by sharing medical costs between you and the insurance company. You pay a monthly premium to keep the plan active, and then the plan applies deductibles, copays, coinsurance, and an out-of-pocket maximum when you receive care.

That is the basic structure, but the details matter. Marketplace plans are grouped into Bronze, Silver, Gold, and Platinum categories. These categories do not measure quality. They mainly show how costs are divided between your monthly premium and what you may pay when you use care. HealthCare.gov explains that all Marketplace plans in each category cover the same essential health benefits, but the cost-sharing differs.

Key Terms to Know

| Term | Simple Meaning |

| Premium | Your monthly payment for the plan |

| Deductible | What you pay before the plan starts sharing more costs |

| Copay | A fixed amount for a visit or prescription |

| Coinsurance | A percentage of the cost you pay after the deductible |

| Out-of-pocket maximum | The most you pay for covered in-network care in a plan year |

Metal Tiers at a Glance

| Tier | Monthly Premium | Cost When You Use Care | Often Best For |

| Bronze | Lower | Higher | People who want lower monthly payments |

| Silver | Moderate | Moderate | People seeking balance, especially if savings apply |

| Gold | Higher | Lower | People who expect regular care |

| Platinum | Highest | Lowest | People who want more predictable out-of-pocket costs |

A simple way to think about it is this: Bronze may help lower your monthly bill, while Gold or Platinum may lower your costs when you actually need medical services.

A person who rarely visits the doctor may feel comfortable with a Bronze plan. A person with regular specialist visits and ongoing prescriptions may save more overall with a Gold plan, even if the monthly premium is higher.

What’s the Difference Between HMO and PPO Plans in Texas?

An HMO usually gives you a narrower network and often requires referrals for specialist care. A PPO usually gives you more flexibility and may allow out-of-network care, but it often comes with higher premiums.

This is one of the most important parts of plan selection because network rules affect both convenience and cost. HealthCare.gov explains that some Marketplace plan types restrict provider choices, while others pay a greater share for out-of-network care.

| Feature | HMO | PPO |

|---|---|---|

| Primary care role | Usually central | Usually less restrictive |

| Specialist referrals | Often required | Usually not required |

| Out-of-network coverage | Usually very limited except emergencies | Usually available at higher cost |

| Premium level | Often lower | Often higher |

| Flexibility | Lower | Higher |

Someone in Farmers Branch who already sees a Dallas specialist may prefer a PPO if that doctor is not included in an HMO network. The lower HMO premium may not feel worth it if it forces a provider change.

If you are still weighing your options, our guide on HMO, PPO, EPO, and POS health plans in Dallas breaks down each plan type so you can compare them more clearly before deciding.

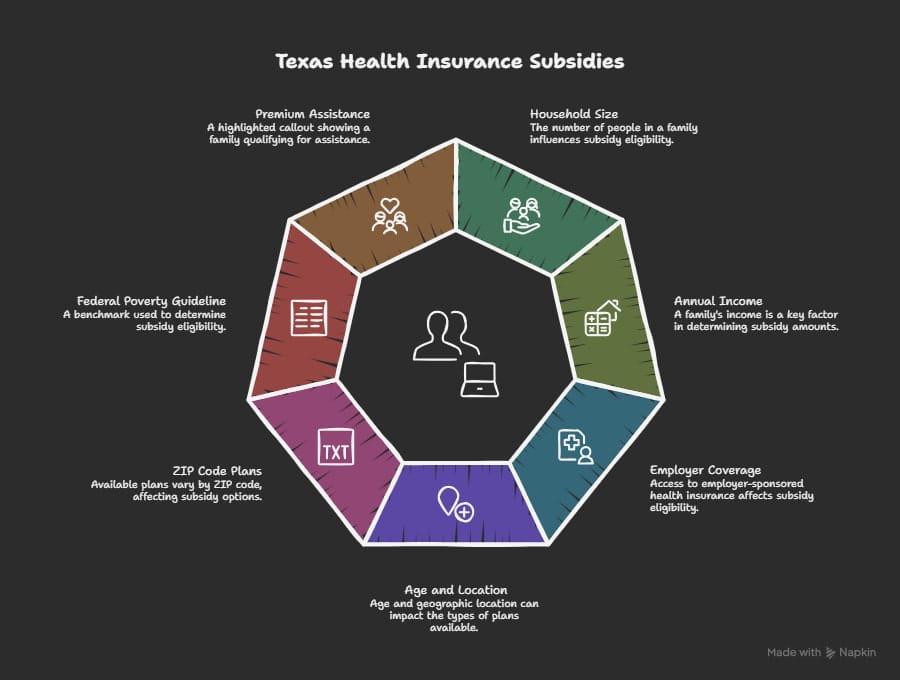

Am I Eligible for Subsidies or Premium Tax Credits in Texas?

Yes, many Texans may qualify for Marketplace savings, even if they do not think of themselves as low income. Premium tax credits are based on factors such as household size, income, and whether you have access to other affordable coverage.

This is why many people benefit from checking before making assumptions. HealthCare.gov is the federal Marketplace used in Texas, and it allows applicants to estimate whether they qualify for financial help.

For 2026, the federal poverty guideline for the 48 contiguous states and D.C. is $15,650 for one person and $32,150 for a household of four. Those figures are part of the affordability framework used to determine eligibility for Marketplace savings.

What Affects Subsidy Eligibility?

- household size

- annual household income

- access to employer-sponsored coverage

- age and location

- available plans in your ZIP code

Quick Reference Table

| Household Size | 2026 Federal Poverty Guideline |

| 1 | $15,650 |

| 4 | $32,150 |

The important point is that subsidy eligibility is not just about income in isolation. Household details and local plan pricing matter too.

A Texas family of four earning around $60,000 may qualify for premium assistance depending on the exact household setup and available local plans. That could significantly reduce the monthly premium compared with the full listed price.

When Can I Actually Enrol or Change My Health Insurance in Texas?

You can usually enroll during Open Enrollment, or outside that window if you qualify for a Special Enrollment Period. For Marketplace coverage, Open Enrollment generally runs from November 1 to January 15, with December 15 usually being the deadline for coverage that starts on January 1.

Outside Open Enrollment, plan changes and new enrolments are usually limited to people who experience a qualifying life event. HealthCare.gov also notes that outside Open Enrollment, you can enrol or change plans only if you qualify for a Special Enrollment Period.

Common Qualifying Life Events

| Life Event | Why It May Qualify You |

| Losing job-based coverage | You need replacement coverage |

| Getting married | Household status changes |

| Having or adopting a child | Family size changes |

| Moving | Available plans may change |

| Certain income or household changes | Eligibility may shift |

If someone loses employer health insurance in April, they usually do not have to wait until November. That job loss may trigger a Special Enrollment Period and allow them to choose Marketplace coverage sooner.

Does Health Insurance Cover Pre-Existing Conditions and Essential Benefits?

Yes, ACA-compliant Marketplace plans cover pre-existing conditions, and insurers cannot deny you coverage or charge you more because of one. HealthCare.gov clearly states that all Marketplace plans must cover treatment for pre-existing medical conditions.

Marketplace plans also include the essential health benefits required under the ACA. These benefits include preventive services, emergency care, hospitalisation, mental health care, prescription drugs, and more. HealthCare.gov explains that all Marketplace plan categories cover the same essential health benefits, including preventive services.

Core Essential Benefits

- outpatient care

- emergency services

- hospital care

- maternity and newborn care

- mental health and substance use treatment

- prescription drugs

- rehabilitative services

- lab services

- preventive and wellness services

- paediatric services, including children’s dental and vision

That said, covered does not always mean free. A service may still be subject to a deductible, copay, coinsurance, prior authorisation, or network rules.

A person with diabetes can enroll in a Marketplace plan in Texas without being rejected because of that condition. However, they still need to compare how different plans handle insulin, specialist visits, and supply coverage.

How Can a Texas Health Insurance Broker Help Me Compared to Buying Direct?

A Texas health insurance broker helps you compare plans more clearly and spot details that are easy to miss when shopping alone. The biggest value is guidance, not pressure.

Buying direct or using the Marketplace on your own can work, but many people focus too much on premium and not enough on network access, total yearly cost, prescriptions, or plan fit. A broker can help narrow the options based on how you actually use care.

Comparison Table

| Option | Main Advantage | Main Limitation |

| Buying direct from one carrier | Simple if you already know the carrier | You only see one company’s plans |

| Using HealthCare.gov alone | Full Marketplace access | You must compare and interpret everything yourself |

| Using an independent broker | Personal guidance across multiple options | Best for people who want help making sense of the details |

At Wilkerson Insurance Agency in Farmers Branch, that support may include reviewing doctors, prescriptions, deductible exposure, and the trade-off between a lower monthly premium and higher out-of-pocket risk.

A self-employed Texan may see three Silver plans that look almost identical online. A broker may notice that one includes preferred hospitals, another handles prescriptions better, and a third only looks cheaper because it shifts more cost into the deductible.

If you want help comparing Texas plans without doing all the sorting on your own, Wilkerson Insurance Agency in Farmers Branch can walk you through the choices in a simpler and more practical way.

What Are the Biggest Mistakes Texans Make When Choosing Health Insurance?

The biggest mistakes are choosing based only on premium, ignoring provider networks, overlooking prescription coverage, and misunderstanding total yearly cost. These mistakes are common because most people are making a decision quickly under time pressure.

A strong plan is not just the one with the lowest monthly number. It is the one that works well when you actually need medical care. Before locking in a choice, going through ten key questions to ask before picking a health insurance plan can help you avoid the most common errors people make under deadline pressure.

Common Mistakes and Better Alternatives

| Mistake | Why It Causes Problems | Better Approach |

| Choosing only by premium | May hide high out-of-pocket costs | Compare total yearly value |

| Ignoring network details | Preferred doctors may be excluded | Verify doctors and hospitals first |

| Forgetting prescriptions | Drug costs can vary a lot | Check formulary and tiers |

| Missing enrolment timing | May delay access to coverage | Review deadlines early |

| Assuming all Silver or Gold plans are the same | Plan details differ more than people expect | Compare benefits, network, and cost structure |

A person picks the cheapest plan available, then learns their regular doctor is out of network and their prescription falls into a costly tier. The monthly savings disappear once they start using care.

Why Choose Wilkerson Insurance Agency?

Choosing health insurance is not just about finding a plan. It is about finding the right coverage with the right support, so you can make a decision with confidence. That is where working with an experienced local agency can make a real difference.

At Wilkerson Insurance Agency, we focus on making health insurance easier to understand and easier to compare. We help Texans sort through complex choices with more clarity, less stress, and more personal guidance.

- Independent Plan Comparisons: We are an independent agency, which means we are not limited to one carrier. We compare plans from multiple insurance companies to help you review options based on coverage, cost, and provider access.

- Personalised One-to-One Guidance: Every person and family has different needs. We take time to understand your budget, healthcare priorities, doctor preferences, and long-term goals before helping you compare plans.

- Experienced Texas Insurance Support: We have been serving Texans since 2010 and understand how health insurance works across different situations, including individual coverage, family plans, Medicare-related options, and small business needs.

- Help Beyond Enrolment: Our support does not stop after you choose a plan. We also help clients with paperwork, plan questions, and ongoing guidance, which is especially helpful when coverage needs change later.

- Friendly, Clear Explanations: Health insurance terms can be overwhelming, but our goal is to explain things in a way that feels simple and practical. We want you to understand what you are choosing, why it matters, and how it may affect your real healthcare costs.

Conclusion

Health insurance choices become much easier when you answer the most important questions first. What will the plan cost each month, what could it cost when you actually use care, are your doctors in network, and do you qualify for savings?

Those answers matter more than simply chasing the lowest premium. In Texas, many people qualify for Marketplace help, pre-existing conditions are protected under ACA-compliant plans, and enrollment timing matters more than many people realise. You can check your eligibility and browse available plans directly on HealthCare.gov, the federal Marketplace used across Texas.

Wilkerson Insurance Agency in Farmers Branch has spent years helping Texans compare options with more clarity and less stress. When the details feel confusing, having a guide can make the entire process easier to understand. If you want to understand how premium tax credits are calculated, the IRS guidance on premium tax credits provides a clear breakdown of the rules and eligibility basics.

Ready for clear, personalised answers? Contact Wilkerson Insurance Agency in Farmers Branch, TX, call 214-501-9613, and request your free Texas health insurance quote today.