How much does home health care insurance cost per month in Texas? In most cases, it depends on your age, health, and policy design, but for many people, the monthly premium is far lower than paying for home care out of pocket. That is why this topic matters for families planning ahead.

If you are searching for home health care insurance cost per month in Texas, you likely want to know both the insurance premium and the real cost of care at home. In Texas, home health care can cost thousands per month, so understanding your options early can help you avoid financial pressure later.

Wilkerson Insurance Agency has been helping Texas families since 2010 with personalised, unbiased insurance guidance. As an independent agency in Farmers Branch, we compare multiple carriers, explain coverage clearly, and help you choose a plan that fits your budget and long-term needs.

In this guide, you will learn:

- how much home health care can cost per month in Texas

- what long-term care insurance may cost at different ages

- what Medicare covers and where the biggest gaps are

- how Texas Partnership policies can help protect assets

- what factors change your premium and long-term value

- when it may make sense to buy coverage before costs rise further

What Is the Real Monthly Cost of Home Health Care in Texas Right Now?

The short answer is that home health care in Texas is expensive enough to create a real financial problem for many families. Recent Texas cost data shows home health aide care at $68,640 per year, which works out to about $5,720 per month. Homemaker services are slightly lower at $64,064 per year, or about $5,339 per month.

That matters because people often focus on the monthly insurance premium first, when the bigger number is usually the care bill itself. A premium of $100 to $300 a month looks very different when the alternative is paying $5,000 or more every month from savings, retirement income, or family support. For families already managing complex care situations, our resource on benefits of home healthcare plans for seniors with complex needs in Dallas shows how the right policy can absorb much of that financial pressure.

If a parent in Dallas needs ongoing help at home for 12 months, and the average monthly cost is around $5,720, the yearly total is about $68,640. That is enough to drain a large part of many households’ emergency savings or retirement funds.

Texas home care cost snapshot

| Care type | Annual median cost in Texas | Estimated monthly cost |

| Homemaker services | $64,064 | $5,339 |

| Home health aide | $68,640 | $5,720 |

How Much Do Home Health Aides Charge Per Hour in Texas Cities?

City pricing changes the picture. Texas statewide averages are useful, but local markets can be lower or much higher. Dallas is around $5,720 per month, Plano around $4,862, Houston around $4,576, San Antonio around $5,529, and Austin around $7,245.

That is why a generic national article often feels incomplete. You do not pay the national average. You pay what agencies charge in your part of Texas.A family in Plano may face a monthly cost under $5,000, while a similar care need in Austin may cost well above $7,000. The policy amount that feels sufficient in one city may feel thin in another.

| Texas city | Estimated monthly home health care cost |

| Houston | $4,576 |

| Plano | $4,862 |

| San Antonio | $5,529 |

| Dallas | $5,720 |

| Austin | $7,245 |

Does Medicare Cover Home Health Care in Texas – and What Are the Gaps?

Yes, Medicare covers some home health care, but not the kind of long-term everyday support many families expect. Medicare covers home health services when they are medically necessary and when you meet eligibility rules, including being homebound and needing part-time or intermittent skilled services.The problem is the gap. Medicare does not pay for 24-hour home care, meal delivery, homemaker services unrelated to your care plan, or custodial and personal care when that is the only care you need. It also does not provide general long-term care coverage for ongoing daily support.

This is where many families get surprised. They hear “home health” and assume that help with bathing, dressing, supervision, and meal support will all be covered. In reality, Medicare is much narrower than that. Our post on how Medigap fills the costly gaps in Medicare explains those limits clearly and what supplemental options can and cannot do for long-term home care.

If your mother is homebound after an illness and needs skilled nursing visits and therapy for a short period, Medicare may help. But if six months later she mainly needs help bathing, dressing, walking around the house, and staying safe, Medicare may not cover those ongoing personal care costs.

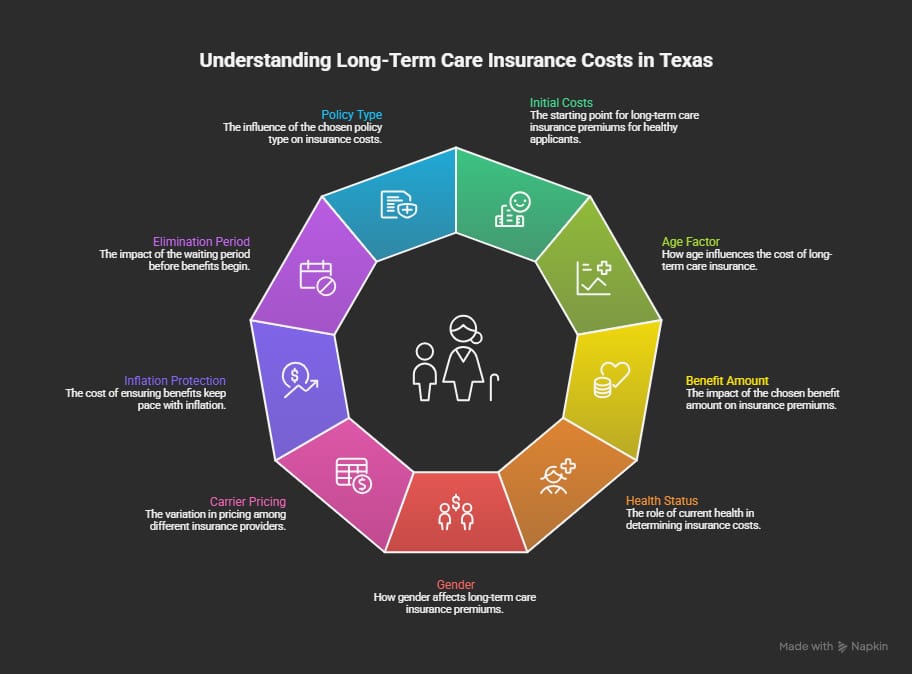

How Much Does Long-Term Care Insurance Cost Per Month in Texas in 2026?

Long-term care insurance in Texas often starts in the low hundreds per month for healthier applicants who buy earlier, but premiums rise with age and richer benefits. AALTCI benchmark figures show that a single male age 55 paid about $1,200 annually on average in more recent reporting, while a single female age 55 paid about $1,750 to $2,800 annually, depending on the dataset and inflation assumptions. That works out to roughly $100 to $233 per month. At age 60, those numbers rise further.

The exact monthly premium in Texas depends on:

- age when you apply,

- current health,

- gender,

- carrier pricing,

- daily or monthly benefit amount,

- inflation protection,

- elimination period,

- and whether the policy is traditional or Partnership-qualified.

So the better way to think about pricing is not “What is the average?” but “What would a policy cost for someone my age and health with enough benefits to actually help in my Texas market?”

A healthy buyer in the mid-fifties may find coverage near the low hundreds per month. A buyer in the mid-sixties wanting stronger benefits and inflation protection may see much higher pricing. That difference is one reason early planning matters. Our resource on planning for the unexpected and long-term care needs before age 65 puts the timing question into sharper focus with national data.

Sample premium comparison

| Buyer profile | Approximate annual premium | Approximate monthly premium |

| Single male, age 55 | $1,200 to $1,750 | $100 to $146 |

| Single female, age 55 | $1,750 to $2,800 | $146 to $233 |

| Single male, age 60 | about $2,060 | about $172 |

| Single female, age 60 | about $3,325 | about $277 |

These are benchmark figures, not guaranteed Texas quotes.

How Age, Health, and Benefit Amount Change Your Premium

Buying later usually costs more, and health problems can make coverage harder to get. AALTCI-based data shows that premiums rise noticeably between age 55 and 60, and again at 65.

Health matters just as much. Underwriting often looks at prescriptions, diagnoses, mobility, and cognitive concerns. The stronger your health at the time of application, the more likely you are to qualify and the better your pricing is likely to be.

Benefit design matters too. A larger monthly benefit, stronger inflation protection, and longer benefit period will usually increase the premium.

Kathryn Gabbert buying at 55 with moderate benefits may pay close to $100 to $150 a month. That same person, applying at 65 after health changes, may face a much higher premium or fewer available choices.

How Can Long-Term Care Insurance Actually Lower Your Home Health Care Bills?

Long-term care insurance can reduce how much of the care bill comes from your own savings. It does this by paying toward covered long-term care expenses once the policy conditions are met, such as the elimination period and benefit triggers. If you want a plain-language look at why this coverage matters at a family level, our guide to the life-changing benefits of choosing a home health care plan walks through the value from a long-term planning perspective.

This matters because the gap between a premium and an actual care bill can be huge. A premium of $150 or $250 per month is small compared with paying $5,720 a month out of pocket for home health aide services in Texas.

Betty Wong’s family self-paying $5,720 per month would spend about $68,640 in a year. If a policy helps offset a large share of that cost after the waiting period, the household may preserve tens of thousands of dollars that would otherwise come straight from retirement savings or home equity.

Simple cost comparison

| Scenario | Estimated monthly out-of-pocket impact |

| No coverage, paying full Texas average | $5,720 |

| Paying only a policy premium before care is needed | roughly $100 to $277 in sample benchmark cases |

What Is the Texas Long-Term Care Partnership Program and Why It Matters

The Texas Long-Term Care Partnership Program gives you more than standard coverage. Its biggest advantage is asset protection. For every dollar your qualifying policy pays in benefits, Medicaid can disregard one dollar of your assets if you later need to apply for Medicaid long-term care support.

That is important because many people worry about having to spend down savings before qualifying for Medicaid. A Partnership policy can reduce that pressure by protecting part of what you have built. Our post on tailored home healthcare plans and controlling rising costs covers how to structure a policy around specific asset protection goals.

Texas Partnership policies also require inflation protection and include extra consumer protections compared with non-Partnership policies.

If your Partnership-qualified policy pays $150,000 in benefits over time, Medicaid may disregard $150,000 of your assets if you later need to qualify. That can help protect savings that might otherwise have to be spent first.

Why it matters in Texas

| Partnership feature | Why it helps |

| Dollar-for-dollar asset disregard | Helps protect assets if Medicaid is needed later |

| Required inflation protection | Helps benefits keep pace with rising care costs |

| Added consumer protections | Gives stronger planning value than a basic policy |

Is Long-Term Care Insurance Worth It in Texas Given Today’s Care Costs?

It can be worth it if you want to protect savings, reduce pressure on family, and avoid paying large care bills entirely on your own. It tends to be most valuable for people who are not wealthy enough to self-fund care comfortably for years, but who also do not want to rely only on future Medicaid eligibility. Our post on why home health care plans are a smart investment for aging in place in Dallas explores that trade-off from a longer-term planning angle.

It may be less important if you have enough liquid assets to pay for years of care without affecting your spouse, lifestyle, or legacy goals. But for many middle-income and upper-middle-income Texas families, the real question is not whether care is expensive. It clearly is. The question is whether they want to transfer part of that risk before they need care.

If you expect to retire with moderate savings and want to protect your spouse from a long stretch of home care bills, coverage may be worth serious consideration. If you can easily absorb $70,000 to $100,000 a year in future care costs without changing your plans, the calculation may be different.

Other Ways to Help Pay for Home Health Care in Texas

There are other ways to pay, but each has limits. Medicare helps only in narrow medical situations. Medicaid may help later if you meet eligibility requirements. Some veterans may qualify for benefits depending on their service and care situation. Personal savings, annuities, and coordinated family support may also play a role.

The challenge is that none of these options works perfectly for everyone. That is why planning usually works best when you understand which funding source covers which type of need.

A family may use Medicare for short-term recovery care after an illness, rely on personal savings for immediate expenses, and use long-term care insurance to help with a later extended care need that Medicare does not cover.

Why Choose Us

Choosing home health care coverage is not just about finding a low premium. You also need to know whether the policy gives you real protection when care is needed. That is where the right guidance matters.

At Wilkerson Insurance Agency, we help Texas families compare options with clarity and confidence. Here is why clients choose us:

- Independent comparisons

We are not tied to one carrier, so you can review multiple options side by side. - Personalised guidance

We match coverage to your age, health, budget, and future care goals. - Texas experience since 2010

We understand local needs, care costs, and the insurance concerns Texas families face. - Support beyond enrollment

We help with paperwork, questions, and ongoing policy support after signup. - Clear explanations

We simplify complex insurance terms so you can make informed decisions without confusion.

For official details on how the Texas Partnership Program works, the Texas Health and Human Services Long-Term Care Partnership page explains eligibility, asset protection rules, and how qualifying policies are structured.

For independent benchmarking of long-term care insurance costs at different ages, the American Association for Long-Term Care Insurance cost guide publishes data-backed premium ranges that can help you frame realistic expectations before requesting a personalized Texas quote.

Frequently Asked Questions

What is the average home health care insurance cost per month in Texas?

There is no single statewide average because pricing depends on age, health, gender, and benefit design. For many healthier buyers in their fifties and early sixties, benchmark premiums often land in the low hundreds per month, but stronger coverage can cost more.

How much is long-term care insurance per month for a 55-year-old in Texas?

A healthy 55-year-old may see sample benchmark premiums from roughly $100 to over $200 per month, depending on gender and policy structure. Actual Texas quotes may be lower or higher depending on underwriting and benefits.

Does Medicare pay for home health aides in Texas?

Medicare may cover limited home health aide services when you also qualify for covered skilled care and meet homebound rules. It does not cover long-term custodial care when personal care is the main need.

What does the Texas Long-Term Care Partnership Program protect?

It protects assets through dollar-for-dollar asset disregard. If your qualified policy pays benefits, Medicaid can disregard an equal amount of your assets if you later apply for long-term care support.

How much does in-home care cost per month without insurance in Dallas?

Dallas is around $5,720 per month for home health care based on recent Texas figures, though actual agency rates vary. That is why many families look at insurance before care is needed.

Can Medicare Supplement plans cover long-term home care?

No. Medigap helps with certain Medicare cost-sharing amounts for Medicare-covered services, but it does not turn noncovered long-term custodial care into a covered benefit.

Conclusion

The key point is simple. Long-term care insurance premiums in Texas are often far smaller than the cost of paying for home health care out of pocket. Many buyers may see premiums in the low hundreds per month, while actual home health care in Texas can run around $5,720 monthly and even higher in some cities. Medicare helps in limited medical situations, but it does not cover most long-term personal care needs.

If you want help comparing real options, contact Wilkerson Insurance Agency in Farmers Branch, Texas for a personalized review. You can request a free quote, call 214-501-9613, and compare plans that fit your budget, health, and long-term goals before care costs become urgent.