For most people, the answer is that disability income insurance usually costs around 1% to 3% of your annual income, but your actual monthly premium depends on your age, health, occupation, benefit amount, waiting period, and policy features. So even if two people earn the same income, their monthly cost can still look very different.

That is exactly where expert guidance matters. At Wilkerson Insurance Agency, we help Texans compare disability income coverage with clarity, not confusion. As an independent insurance agency based in Farmers Branch, TX, we are not tied to just one carrier. That means you get unbiased guidance, side-by-side comparisons, and help choosing coverage that fits your budget, work style, and long-term financial needs. Since 2010, we have helped thousands of clients across Texas understand complex insurance decisions in a simpler, more practical way.

When you read this guide, you will understand:

- what disability income insurance may cost per month in Texas

- which factors raise or lower your premium

- how occupation, income, and policy structure affect pricing

- whether individual or group disability coverage makes more sense

- how self-employed Texans can compare options more wisely

- which riders may be worth adding and which may not

- how to avoid paying for coverage that looks cheap but leaves important gaps

How Much Does Disability Income Insurance Cost Per Month in Texas?

The clearest starting point is the 1% to 3% rule. That is the range commonly used for long-term disability insurance, and it gives you a useful way to estimate your likely monthly premium before you request quotes. Policygenius states that long-term disability insurance usually costs between 1% and 3% of your income.

Here is what that often looks like in monthly dollars:

| Annual Income | Estimated Monthly Cost | Estimated Yearly Cost |

| $50,000 | $42 to $125 | $500 to $1,500 |

| $75,000 | $63 to $188 | $750 to $2,250 |

| $100,000 | $83 to $250 | $1,000 to $3,000 |

| $125,000 | $104 to $313 | $1,250 to $3,750 |

| $150,000 | $125 to $375 | $1,500 to $4,500 |

| $200,000 | $167 to $500 | $2,000 to $6,000 |

These are estimate ranges, not guaranteed quotes. They help you budget, but they do not replace an actual application. The final price depends on the details of your policy and your personal risk profile.

A simple example makes this easier to understand. If you earn $100,000 a year and want long-term coverage, you may expect a monthly premium somewhere between $83 and $250. But if you work in a low-risk office role, are healthy, and choose a longer waiting period, your premium may stay near the lower end. If you are older, self-employed, or want richer benefits, it may move much higher.

Quick Cost Snapshot by Income Level

The chart below gives you a faster way to picture how pricing changes as income rises.

| Income Level | Lower-End Cost | Mid-Range Cost | Upper-End Cost |

| $75,000 | $63 | About $125 | $188 |

| $100,000 | $83 | About $167 | $250 |

| $150,000 | $125 | About $250 | $375 |

| $200,000 | $167 | About $333 | $500 |

This is useful because many readers want a quick answer before they dig into details. The pattern is simple: the more income you protect, the more the premium tends to rise. Still, the coverage design matters just as much as salary.

Cost Examples by Common Texas Occupations

Occupation is one of the biggest pricing factors. Insurers view some jobs as safer and more stable than others. Lower-risk office work often costs less to insure, while more physical or higher-risk work usually costs more. Policygenius lists occupation as a major factor in disability insurance pricing.

Here is a simple comparison for Texans aiming for a policy that protects around $5,000 per month in income:

| Occupation | General Risk Level | Usual Premium Direction |

| Office administrator | Low | Lower end |

| Accountant | Low | Lower end |

| Real estate agent | Moderate | Low to middle |

| Small business owner | Moderate, depends on duties | Middle |

| Contractor | High | Upper end |

| Construction worker | High | Upper end |

That does not mean every person in the same occupation pays the same amount. Insurers also care about your actual day-to-day duties. A small business owner who mainly works at a desk may be priced differently than one who handles field work, deliveries, or site inspections.

For example, a Dallas real estate agent and a Farmers Branch accountant might both earn $110,000 a year. The accountant may qualify for a lower premium because the role is viewed as less physically risky. The real estate agent may still get affordable coverage, but constant driving, commission-based work, and the need to stay active in the field can affect pricing.

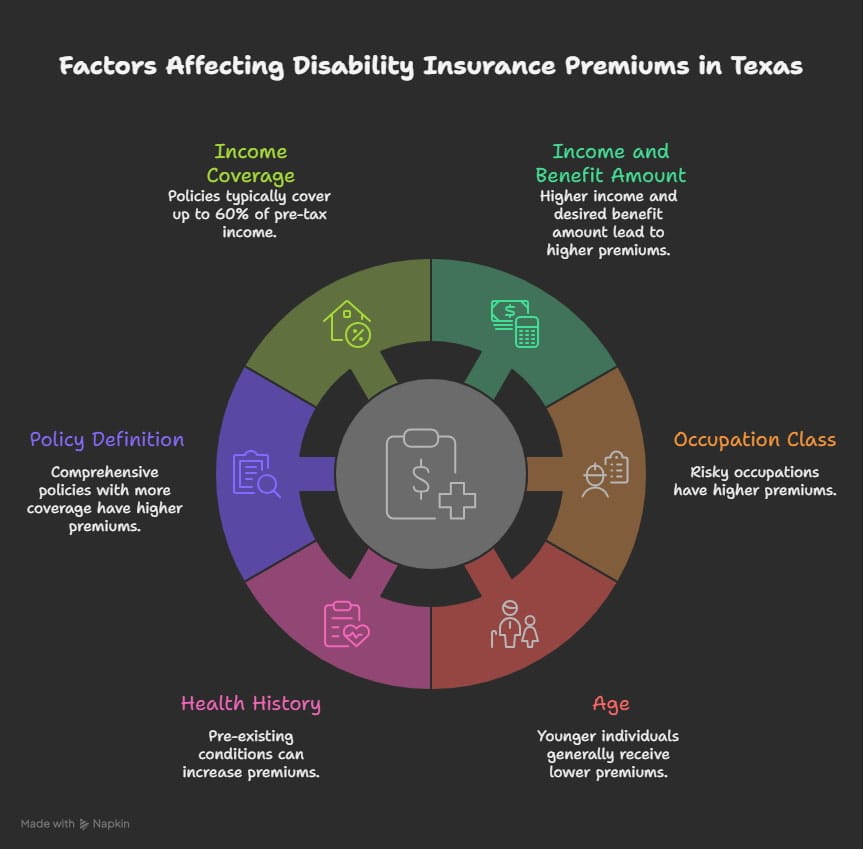

What Factors Most Affect Your Disability Insurance Premium in Texas?

If you want the second direct answer, here it is: your premium is mainly shaped by income, occupation, age, health, elimination period, benefit period, and policy definition. Once you understand these, the quote makes much more sense.

Here are the biggest pricing factors:

1. Income and monthly benefit amount

The more income you want to replace, the more the policy usually costs. Disability insurance normally replaces only part of your income, not all of it. Policygenius notes that many policies cover up to about 60% of pre-tax income.

A person earning $60,000 a year usually needs less coverage than someone earning $180,000, so the second person will usually pay more.

2. Occupation class

Low-risk desk jobs are usually cheaper to insure than physically demanding jobs. This is one of the most important pricing differences in Texas, especially for contractors, service workers, and self-employed professionals.

A bookkeeper and a roofer with similar incomes will not be priced the same, because the risk of being unable to work is higher in the more physical occupation.

3. Age

Older applicants usually pay more than younger ones. Buying early often helps you lock in lower pricing.

Example:

A healthy 30-year-old usually gets a better rate than a healthy 50-year-old applying for similar benefits.

4. Health history

Medical conditions can raise premiums, add exclusions, or affect approval. This is why comparing more than one carrier matters.

Example:

A person with a history of back issues may see more restrictions than someone with no major medical history.

5. Policy definition

A broader definition of disability usually costs more because it can pay under more situations.

A specialised professional may pay extra for stronger protection that covers the inability to do their exact job, not just any job.

How Elimination and Benefit Periods Change Your Monthly Cost

This is one of the easiest places to control your premium. A longer elimination period usually lowers your monthly cost, while a longer benefit period usually raises it. The Texas Department of Insurance explains that disability policies have a waiting period before benefits start, and that short-term and long-term policies differ mainly in how long they pay.

Here is a simple comparison:

| Policy Feature | Lower Monthly Cost | Higher Monthly Cost |

| Elimination Period | 90 to 180 days | 30 days |

| Benefit Period | 2 to 5 years | To age 65 |

Think of the elimination period as the amount of time you must cover on your own before benefits begin. If you have strong savings, you may be able to wait longer and lower the premium. If you do not have much in emergency savings, paying more for a shorter waiting period may be the safer move.

A self-employed consultant in Dallas has six months of savings. That person may choose a 180-day elimination period to reduce premium. Another person living paycheque to paycheque may need a 30-day elimination period because they cannot absorb months without income.

Is Individual or Group Disability Insurance Better for Texans?

Group coverage is often cheaper, but individual coverage is usually more flexible and portable. The better choice depends on whether you already have disability insurance through work and whether that protection would still be enough if your job changed.

The Texas Department of Insurance says some employers offer disability insurance, and if they do not, you can buy it yourself. That is especially relevant for self-employed Texans, freelancers, real estate professionals, and small business owners.

Here is the comparison:

| Feature | Group Coverage | Individual Coverage |

| Cost | Usually lower | Usually higher |

| Portability | Often tied to your job | Usually stays with you |

| Customisation | Limited | More flexible |

| Best for | Employees with solid benefits | Self-employed people, professionals, business owners |

Group coverage is not bad. In fact, it can be a strong starting point. The problem is that some people assume it is enough when it really is not.

A Dallas employee may receive basic group disability coverage through work. It sounds helpful, but the monthly benefit cap may not cover the mortgage, childcare, and daily living costs.

In that case, adding an individual policy may fill the gap more effectively. For a fuller breakdown of how these plans are structured, our guide on understanding disability income plans in Dallas covers the key components worth knowing before you decide.

Why Self-Employed Texans Often Pay More, and How to Lower the Cost

Self-employed Texans often pay more because their income may be harder to document, their job duties can vary, and they usually do not have employer-paid benefits backing them up. At the same time, they often need disability protection more than salaried employees because their income may stop the moment they cannot work.

This applies to many Texas professionals, including:

- real estate agents;

- contractors;

- freelancers;

- consultants;

- small business owners.

There are three common ways to lower cost without making the policy weak:

| Strategy | Why It Helps |

| Choose a longer elimination period | Lowers monthly premium |

| Compare multiple carriers | Helps you find better value |

| Limit unnecessary riders | Keeps the policy focused |

A Farmers Branch small business owner first asks for the cheapest available plan. That quote looks attractive, but the benefit period is short and the contract leaves gaps. After comparing options, the owner may choose a slightly higher premium with stronger long-term protection.

In real life, that better fit can be far more valuable than saving a few dollars a month. Our guide on how to choose the best disability income plan in Dallas walks through the key comparison points so you know exactly what to look for.

If you want a side-by-side comparison without the pressure of being pushed into one carrier, Wilkerson Insurance Agency in Farmers Branch, TX can help you review options based on your income, work type, and budget.

Should You Add Riders? Common Ones and Their Cost Impact

Riders can improve your protection, but they also raise your premium. The smart approach is not to add every rider. It is to add the ones that solve a real risk in your life.

Here are some common riders:

| Rider | What It Does | Usual Cost Effect |

| Cost of living adjustment | Helps benefits keep pace with inflation | Raises premium |

| Residual or partial disability | Pays if you can still work but earn less | Raises premium |

| Future purchase option | Lets you increase coverage later in many cases | Raises premium |

These riders are helpful because disability does not always mean total inability to work. Sometimes you can work fewer hours, earn less, or face long-term inflation that reduces the value of your monthly benefit.

A 34-year-old Texas professional expects income growth over the next 10 years. A future purchase option may make sense because it can allow more coverage later without fully starting over.

How an Independent Texas Broker Can Help You Get Better Coverage

The best reason to use an independent broker is simple: they can compare multiple options instead of selling one carrier’s version of the truth. Policygenius also recommends comparing quotes to see whether you are paying too much for coverage.

That comparison matters because disability insurance is not just a price product. It is also a contract product. Two plans may look similar in price but be very different in the details. If you are still learning the basics, our disability insurance 101 guide explains the core terms and what to watch for in a policy before you start comparing.

A broker can help you compare:

- monthly premium;

- waiting period;

- benefit period;

- policy definition;

- rider value;

- portability if your job changes.

A Texas real estate agent may be shown two policies with similar monthly costs. One looks cheaper at first glance, but it has weaker terms. The second policy may cost slightly more while offering stronger partial disability protection and a better long-term safety net. Without a careful comparison, that difference is easy to miss.

Why Choose Us for Disability Income Insurance Guidance in Texas?

Choosing disability income insurance is not only about finding a lower monthly premium. It is about choosing coverage that can actually protect your income when you need it most. At Wilkerson Insurance Agency, we help make that decision easier by comparing real options and explaining them in plain language.

- Independent Carrier Comparisons: As an independent agency, we compare plans from multiple carriers instead of pushing one company’s policy. That helps you find coverage that fits your budget and needs.

- Personalised Guidance: We look at your income, occupation, and goals before recommending options. This helps you choose a policy that fits your real situation.

- Texas Experience Since 2010: We have helped Texans since 2010, including individuals, families, self-employed professionals, and small business owners across Texas.

- Help Beyond the Quote: We help with comparisons, paperwork, enrollment, and ongoing support, so you are not left figuring everything out on your own.

- Clear, Client-First Service: We focus on simple explanations, honest guidance, and helping you feel confident in the coverage you choose.

Frequently Asked Questions

What is the average monthly cost of long-term disability insurance in Texas?

A common estimate is about 1% to 3% of annual income. For someone earning $100,000, that often means roughly $83 to $250 per month.

Does Texas require private disability insurance?

No. Texas does not require private disability coverage. Some employers offer it, and people can also buy their own policies. The Texas Department of Insurance provides additional guidance on individual disability coverage options available to Texas residents.

Is disability insurance taxable?

The IRS says disability benefits from an employer-paid plan are generally taxable. Benefits from a plan you paid for yourself with after-tax dollars are generally not taxable.

Is Social Security disability enough?

Usually not for most working households. SSA data shows that about 1 in 4 of today’s 20-year-olds will become disabled before age 67, and 65% of the private-sector workforce has no long-term disability insurance.

Conclusion

The disability income insurance cost per month in texas is usually manageable, but the real value depends on how well the policy fits your life. Most Texans fall into the broad 1% to 3% income range, yet the final price can shift based on job risk, age, health, waiting period, benefit length, and riders.

That is why the best decision is not to chase the cheapest premium. It is to choose coverage that would actually protect your income if a serious illness or injury kept you from working. A policy that looks cheap now can leave expensive gaps later.

For clear guidance and personalised quotes, contact Wilkerson Insurance Agency in Farmers Branch, TX at 214-501-9613 and explore your options based on your income, occupation, and budget.