If you are planning for your financial future in Texas, two insurance options will likely come up: long-term care insurance and home healthcare insurance. They sound similar but work very differently.

One covers ongoing care with no set end date. The other covers short-term recovery after surgery or illness. Choosing the wrong one can leave you underinsured when it matters most.

At Wilkerson Insurance Agency in Farmers Branch, TX, we help Texas residents understand exactly what each plan covers before they commit.

What Is Long-Term Care Insurance in Texas?

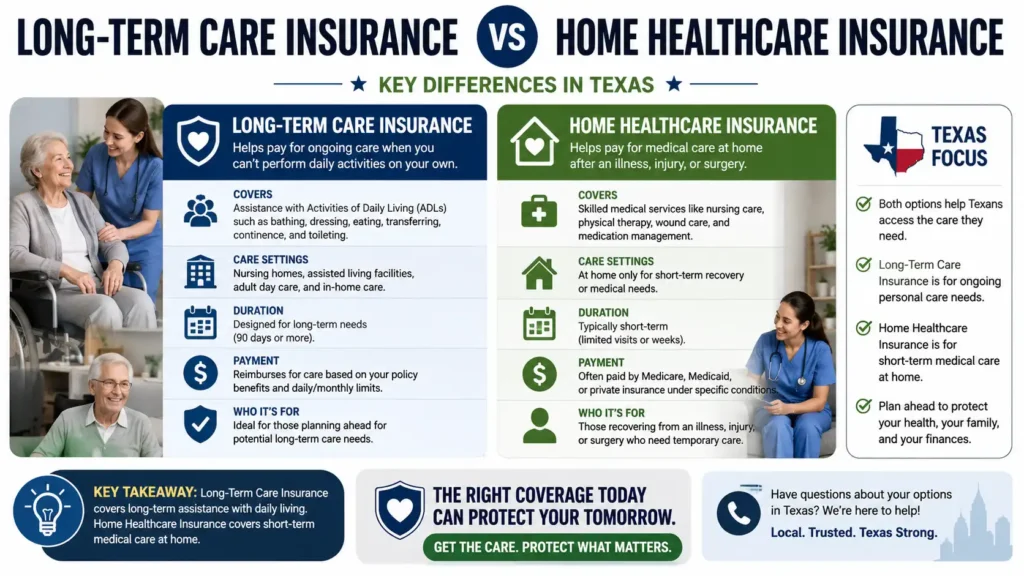

Long-term care (LTC) insurance pays for ongoing personal and medical care when a person can no longer manage daily activities on their own. This care has no set end date.

LTC insurance covers nursing homes, assisted living facilities, memory care units, and in-home care. It activates when a person cannot perform at least two of six Activities of Daily Living (ADLs), such as bathing, dressing, or eating, or when they have a diagnosed cognitive condition like Alzheimer's disease.

In Texas, LTC plans are regulated by the Texas Department of Insurance. Policies can include inflation protection riders to keep benefit amounts in line with rising care costs. The average private nursing home room in Texas costs over $75,000 per year.

Key Features of Long-Term Care Insurance

- Benefits paid daily, weekly, or monthly up to your policy limit

- Covers nursing homes, assisted living, memory care, and in-home care

- Elimination period of 30 to 180 days before benefits begin

- Optional inflation protection

- Triggered by functional or cognitive impairment

LTC insurance is designed for people who anticipate needing extended care, particularly those over 50 planning ahead. Understanding how many Americans face long-term disability by 65 can help you assess your own risk.

What Is Home Healthcare Insurance in Texas?

Home healthcare insurance covers temporary, recovery-focused medical care at home. The goal is to get the patient back to independence.

This coverage applies after hospitalization, surgery, or serious illness. A licensed nurse, aide, or therapist visits the patient at home to provide skilled medical services. Care continues until the patient meets recovery goals or the benefit period ends.

Services may include wound care, medication management, physical therapy, occupational therapy, and vital sign monitoring. Learn more about tailored home healthcare plans that meet individual needs.

Key Features of Home Healthcare Insurance

- Covers short-term, recovery-focused care at home

- Includes skilled nursing visits, therapy, and personal care

- Has a defined benefit period, typically weeks or months

- Generally more affordable than LTC insurance

- Available at any age following a qualifying medical event

Home healthcare insurance fills gaps that standard health insurance and Medicare often do not cover. It is not designed for ongoing care needs. For a comprehensive overview, see our guide on the life-changing benefits of choosing a home health care plan.

Long-Term Care vs Home Healthcare: Core Differences

| Factor | Long-Term Care Insurance | Home Healthcare Insurance |

|---|---|---|

| Duration | Ongoing, no set end date | Short-term, recovery-focused |

| Purpose | Chronic illness, disability, aging | Post-surgery or illness recovery |

| Setting | Home, nursing home, assisted living | Home only |

| Trigger | Cannot perform 2+ ADLs or cognitive decline | Doctor-ordered medical necessity |

| Cost | Higher premiums | Generally lower premiums |

| Typical buyer age | 50 and older | Any age |

The key distinction: LTC insurance is for when someone may not recover their independence. Home healthcare insurance is for when they will.

Wilkerson Insurance AgencyWho Needs Long-Term Care Insurance in Texas?

Most people do not think about long-term care until they need it. By then, pre-existing health conditions can make qualifying difficult or impossible.

The best time to buy an LTC policy in Texas is between ages 50 and 65. Waiting until your late 60s or 70s significantly raises premiums.

Consider LTC Insurance If:

- You have a family history of Alzheimer's, Parkinson's, or similar conditions

- You want to protect retirement savings from care costs

- You want to avoid relying entirely on family members for care

- You prefer to choose your care setting rather than defaulting to Medicaid

Texas Medicaid covers some long-term care, but only after most of your assets are spent down. LTC insurance protects what you have built. Certain life milestones signal it's time to revisit your coverage needs.

Who Needs Home Healthcare Insurance in Texas?

Home healthcare insurance is relevant for anyone facing a recovery period at home. It is not only for older adults.

Younger adults recovering from surgery, injury, or a condition requiring skilled nursing at home can all benefit. Recovery at home is often less expensive than extended hospital stays.

Consider Home Healthcare Insurance If:

- You have planned surgery coming up

- Your standard health insurance has gaps in post-hospitalization home care

- You want to reduce the risk of hospital readmission during recovery

Medicare covers some home health services but has strict eligibility rules and limited duration. Private home healthcare insurance gives you broader, more flexible coverage. For seniors with complex needs, review our guide on benefits of home healthcare plans for seniors.

Cost Comparison in Texas

Average annual premium for a 55-year-old in Texas: $1,500 to $3,000, depending on benefit amount and inflation protection. A policy bought at 65 can cost two to three times more than one bought at 55.

Premiums are generally lower because coverage is time-limited. Standalone plans are more accessible for working-age adults.

Longer benefit periods, higher monthly benefit amounts, shorter elimination periods, inflation protection riders (LTC only), and pre-existing health conditions all increase premiums.

Check our breakdown of home health care insurance costs in Texas for current pricing benchmarks.

An independent broker like Wilkerson Insurance Agency can compare multiple carriers to find the most competitive rate for your situation.

Can You Have Both?

Yes. LTC insurance covers you if care needs become ongoing as you age. Home healthcare insurance covers recovery periods at any stage of life. Together they address different scenarios.

Some LTC policies include a home care benefit, which may reduce the need for a separate home healthcare plan. Review your LTC policy before purchasing additional coverage. Our post on How to choose the right home healthcare plan can help you evaluate your options.

Want help comparing plans?

Wilkerson Insurance Agency can walk through your options at no cost.

Why Wilkerson Insurance Agency

Wilkerson Insurance Agency has served Texas residents from Farmers Branch since 2010, with over 2,000 clients helped across 15 years.

Not tied to one carrier. You get real plan comparisons, not a single-company pitch.

Familiar with state rules on LTC disclosures, inflation protection requirements, and plan structures.

Every recommendation is based on your health history, budget, and goals.

LTC, home healthcare, Medicare supplement, disability income, and life insurance all in one place.

Frequently Asked Questions

Ready to Protect Your Future?

LTC insurance covers ongoing care when someone can no longer live independently. Home healthcare insurance covers short-term recovery at home after a medical event. Let us help you choose the right coverage.

Get Your Free Consultation →Wilkerson Insurance Agency serves Farmers Branch and all of Texas. Call 214-501-9613 or visit wilkersoninsuranceagency.com to compare your options with a licensed advisor. You can also request a quote online.