Between 55 and 64, you are too old for employer coverage to feel secure but too young for Medicare. In Texas, navigating health insurance for ages 55–64 without a clear plan can leave you exposed and overpaying.

Premiums are higher in this age bracket. Pre-existing conditions can limit your options. And the gap between leaving work and turning 65 is longer than most people expect.

Why Is Health Insurance More Expensive Between Ages 55 and 64?

Insurers price premiums based on risk. People in this age range use more healthcare services, so they sit in a higher-risk tier. Under the Affordable Care Act, insurers can charge older applicants up to three times more than younger ones. In Texas, a 60-year-old can expect to pay $600 to $900 per month before subsidies.

Several Factors Drive Your Specific Premium

- Age: The single biggest factor. Costs increase each year after 55.

- Location: Premiums in Dallas-Fort Worth differ from rural Texas counties.

- Tobacco use: Smokers can be charged up to 50% more on ACA plans.

- Plan tier: Bronze, Silver, Gold, and Platinum each carry different cost structures.

- Household income: This determines subsidy eligibility.

One thing that cannot affect your ACA premium: pre-existing conditions. Insurers cannot deny coverage or charge more based on your health history.

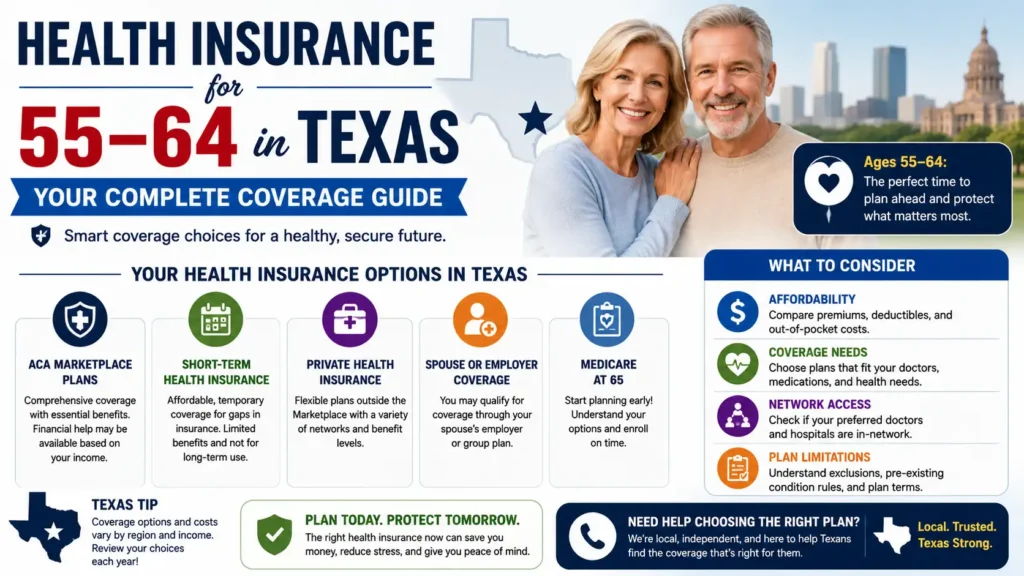

ACA Consumer Protection RulesWhat ACA Marketplace Plans Are Available to Texans 55–64?

Texas uses the federal marketplace at healthcare.gov. Open enrollment runs November 1 through January 15. Job loss, divorce, and other qualifying life events open a 60-day special enrollment window outside that period.

The Four Plan Tiers

Lowest premiums but deductibles of $6,000 to $8,000+. Work for healthy people who want catastrophic protection only. Learn about catastrophic health insurance.

Most important tier for this age group. Only plans that qualify for cost-sharing reductions (CSRs) if income is 100-250% of federal poverty level.

Higher premiums, lower out-of-pocket. Gold often costs less overall than Bronze if you use healthcare regularly. Understanding deductibles helps.

For a complete breakdown, see our HMO vs PPO vs EPO comparison.

Premium Tax Credits

If your household income is below 400% of the federal poverty level, you qualify for premium tax credits. Enhanced subsidies under the Inflation Reduction Act extensions remain available through 2025 for incomes above that level as well.

A 60-year-old in Farmers Branch earning $50,000 per year could reduce a $900 monthly premium to under $400 in many scenarios. This is one of the most underused tools available to early retirees and self-employed Texans.

Premium Tax Credit ExampleWant to see your actual subsidy amount?

We'll run the numbers and find the right plan tier for your situation.

Wilkerson Insurance Agency, based in Farmers Branch, TX, works with clients across the DFW area to identify the right plan tier and run the subsidy numbers before enrollment. Reach out for a personalized review at wilkersoninsuranceagency.com.

How Does COBRA Coverage Work After Leaving a Job?

COBRA lets you continue your employer group coverage for up to 18 months after leaving a job. The problem is cost. You pay the full premium, including the portion your employer previously covered, plus a 2% administrative fee. A plan that cost you $200 per month may run $650 to $800 under COBRA.

COBRA Makes Sense When:

- You are mid-treatment and need to keep your current providers

- You are within a few months of Medicare eligibility

- Marketplace options in your county have limited provider networks

For most people in this age range, an ACA plan with subsidies will be cheaper. You have 60 days from a qualifying event to elect COBRA or enroll in marketplace coverage. Missing that window means waiting until the next open enrollment.

Are Short-Term Health Plans a Good Option in Texas?

Texas allows short-term plans up to 12 months with renewal options. They cost considerably less than ACA plans but do not cover pre-existing conditions, preventive care, mental health, or maternity care in most cases.

Short-term plans work for someone in good health with no ongoing prescriptions who needs coverage for a short, defined period and does not qualify for marketplace subsidies. They are not a good fit for anyone with chronic conditions. An uncovered health event at this age can produce bills that far exceed any premium savings. Learn about the hidden costs of skipping proper health insurance coverage.

Can You Qualify for Medicare Before 65?

Two situations allow early Medicare eligibility:

- SSDI recipients: After 24 consecutive months of Social Security Disability Insurance, you qualify for Medicare regardless of age.

- ESRD or ALS diagnosis: These conditions trigger immediate Medicare eligibility at any age.

For everyone else, Medicare starts at 65. If you are within one to two years of that milestone, start your enrollment planning now. Missing your initial enrollment window creates permanent premium penalties for Parts B and D. Our Medicare Supplement plans page explains what to expect when you transition to Medicare.

What Is a Health Sharing Ministry?

Health sharing ministries are not insurance. Members pool money to share eligible medical costs. In Texas, they operate legally outside insurance regulations.

Monthly costs are lower than ACA plans, sometimes by 30% to 50%. But ministries can decline to share costs for any reason, typically exclude pre-existing conditions for 12 to 36 months, and have no state oversight.

Important: They may work as a short-term bridge for a healthy person with no chronic conditions. For anyone with ongoing health needs, the financial risk is significant.

How to Compare Plans Without Making Costly Mistakes

Critical Comparison Steps

Compare total cost, not just premium. A lower premium usually means a higher deductible. At this age, your total annual cost (premium plus out-of-pocket) is the right number to evaluate. Review our guide on understanding health insurance costs for a complete breakdown.

Confirm your doctors are in-network. Network sizes vary widely across Texas marketplace plans. Before enrolling, check that your primary doctor, specialists, and preferred hospital all accept the plan.

Check the drug formulary. If you take regular medications, verify they are covered and at what cost-sharing level before you commit to a plan.

Run the subsidy calculation. Many Texans in this age group qualify for premium tax credits and never claim them. A self-employed 62-year-old earning $55,000 may save $200 to $400 per month. This should be reviewed every open enrollment.

Act within 60 days of a qualifying event. The enrollment window after losing job-based coverage is firm. Missing it means no coverage until the next open enrollment period.

For a complete checklist, read our post on ten questions to ask before picking a health insurance plan.

Why Wilkerson Insurance Agency Is the Right Choice for Health Insurance in Texas

Wilkerson Insurance Agency is an independent insurance agency in Farmers Branch, TX, serving clients across the Dallas-Fort Worth area.

Not tied to a single carrier. Recommendations are based on what fits your situation, not a commission target.

Deep knowledge of network differences, formulary structures, and cost-sharing details across DFW marketplace plans.

Getting the subsidy calculation right at enrollment means real savings over the full policy year.

Having an agent to call when a qualifying event or claim issue comes up is a practical advantage over buying direct.

Working with an independent agent does not increase your premium. Agents are compensated by the insurer.

Frequently Asked Questions

Get the Right Coverage for Your Age and Budget

For most Texans between 55 and 64, an ACA marketplace plan with premium tax credits is the right starting point. Let us run your subsidy numbers and find the best plan for your situation.

Schedule Your Coverage Review →Wilkerson Insurance Agency serves clients across Dallas-Fort Worth from their office in Farmers Branch, TX. As an independent agency, they compare options across multiple carriers at no added cost to you. Visit wilkersoninsuranceagency.com or call to schedule a coverage review.