Short-term health insurance in Texas offers lower premiums and quick enrollment. That makes it attractive when you are between jobs or waiting for other coverage to start. But before you sign up, you need to understand what these plans cover and where they fall short.

Texas short-term health insurance works well in specific situations. It is not the right fit for everyone. This guide breaks down exactly what you get, what you give up, and when it makes sense.

What Is Short-Term Health Insurance in Texas?

Short-term health insurance is a temporary medical plan for a limited period. In Texas, these plans run from 30 days up to 36 months, and in many cases you can renew back-to-back at the point of sale.

These plans include a deductible, coinsurance, and sometimes copays. However, they are not required to follow Affordable Care Act (ACA) rules. That distinction matters.

Because they fall outside ACA regulations, short-term plans do not have to cover the ten essential health benefits required by marketplace plans. They can deny coverage based on pre-existing conditions and set annual and lifetime benefit limits. This is by design, and it is why premiums are lower.

Short-term plans are available year-round in Texas without a required enrollment period, which is one reason they appeal to people who miss the ACA open enrollment window.

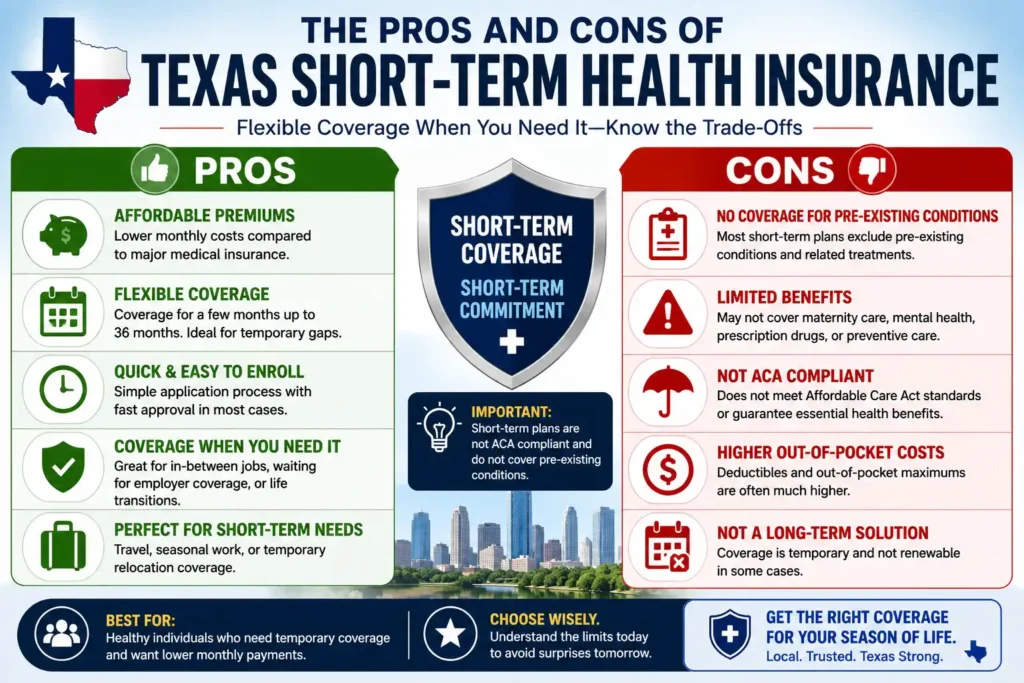

The Pros of Texas Short-Term Health Insurance

Lower Monthly Premiums

Short-term health insurance premiums in Texas can be 50 to 80 percent lower than ACA marketplace plans for a healthy individual.

If you rarely visit the doctor and just want protection against a serious accident or sudden illness, the lower premium may be worth the trade-off.

One client at Wilkerson Insurance Agency was a 29-year-old freelancer between contracts who needed three months of coverage. A short-term plan gave him emergency and hospitalization coverage at about $90 per month. For his situation, it was the right call.

Wilkerson Insurance Agency, Client Case StudyLearn more about affordable health insurance options for self-employed professionals.

Fast Enrollment and Flexible Start Dates

Short-term plans in Texas can be purchased at any time of year. Coverage can often begin the next day after approval, sometimes the same day.

This is a practical benefit for people who:

- Just lost a job and are outside the 60-day special enrollment window

- Aged off a parent's plan and need immediate coverage

- Are waiting for employer coverage to begin at a new job

- Retired early and are not yet eligible for Medicare

Choice of Plan Design

Short-term plans give you more control over plan design than most ACA plans. You can choose your deductible level, coinsurance percentage, and benefit maximum based on your budget and risk tolerance.

Coverage During Transition Periods

Short-term insurance is built for transitions. Between jobs, between school and career, recently divorced, or new to Texas without coverage lined up, these plans serve a specific and legitimate purpose. They are also useful if you missed ACA open enrollment and need coverage before the next window. For more alternatives, see our guide on exploring beyond-the-marketplace individual health insurance options.

The Cons of Texas Short-Term Health Insurance

Pre-Existing Conditions Are Not Covered

Short-term health plans in Texas can deny your application based on medical history, and they do not cover treatment for pre-existing conditions.

If you have diabetes, heart disease, asthma, a recent cancer diagnosis, or a prior surgery, any related treatment will likely be excluded. Unlike ACA plans, short-term insurers are not required to cover pre-existing conditions.

Medical underwriting is involved. Any condition you have been treated for or diagnosed with in the past two to five years may be considered pre-existing and excluded.

No Coverage for Essential Health Benefits

ACA marketplace plans must cover ten essential health benefits. Short-term plans do not. That means little or no coverage for:

- Mental health and substance use treatment

- Maternity and newborn care

- Preventive care and wellness visits

- Prescription drugs

- Pediatric services

If you are pregnant, managing a mental health condition, or take regular medications, a short-term plan is the wrong choice. Our post on why mental health coverage in group plans is a must explains the importance of comprehensive mental health benefits.

Benefit Caps and Annual Limits

Short-term plans set limits on how much they will pay out. Some cap benefits at $250,000 or $500,000 per year. A serious illness or major injury can exceed those limits quickly, leaving you responsible for the rest.

Always check the maximum benefit before purchasing. Plans vary widely. Understanding the hidden costs of skipping proper health insurance coverage can help you evaluate the real financial risk.

No Guaranteed Renewal

Short-term plans do not guarantee renewal. If you develop a health condition while on a short-term plan, you may not be able to renew, or the new condition may be excluded at renewal. Each new term typically involves a fresh application and underwriting review.

Surprise Billing Risk

Short-term plans are not subject to all ACA consumer protections, including some surprise billing rules. Out-of-network care, even in an emergency, may result in costs your plan does not fully cover. Review the network carefully before enrolling.

How Much Do Short-Term Health Plans Cost in Texas?

Costs vary by age, health, deductible, and plan design. General benchmarks:

| Age Group | Estimated Monthly Premium |

|---|---|

| 20s | $50 to $120 |

| 30s | $80 to $175 |

| 40s | $120 to $250 |

| 50s | $200 to $400 |

By comparison, ACA Silver plans for a 40-year-old in Texas without a subsidy run $400 to $600 per month. If you do not qualify for a subsidy and are healthy, the cost difference is significant.

If you do qualify for an ACA subsidy, check your eligibility before defaulting to a short-term plan. Subsidized ACA coverage can be very affordable and offers far broader protection. Our comprehensive guide on understanding health insurance costs breaks down all the factors that affect your premium.

Want help comparing options?

Wilkerson Insurance Agency works with multiple carriers at no cost to you.

When Does Short-Term Health Insurance Make Sense in Texas?

Short-term coverage is the right tool in specific situations. It is not a replacement for comprehensive health insurance.

Good Use Cases

- Between jobs and COBRA costs are too high

- Missed ACA open enrollment and need coverage until the next window

- Healthy, rarely need care, and want basic catastrophic protection

- Waiting 60 to 90 days for employer coverage to begin

- New to Texas and need temporary coverage while sorting out permanent options

For those who need true catastrophic protection with ACA benefits, review our guide on catastrophic health insurance in Texas.

Not a good fit if: You have ongoing health conditions or take regular medications, you are pregnant or planning a pregnancy, you need mental health or substance use treatment, you want preventive care covered, or you need long-term, permanent coverage.

To avoid common pitfalls, read our post on 10 mistakes people make when buying individual health insurance.

Why Wilkerson Insurance Agency Is the Right Choice for Texas Health Insurance

Wilkerson Insurance Agency has been helping Texas residents find health coverage since 2010. We are a licensed broker based in Farmers Branch, TX.

We work with multiple carriers and show you real options.

We know the short-term plan rules, reputable carriers, and where coverage gaps appear.

You work directly with an agent who understands your situation before making a recommendation.

If short-term is not the right fit, we can show you ACA, individual, or family plans in the same conversation.

We know the Texas market and the nuances a national comparison site will not tell you.

Frequently Asked Questions

Ready to Compare Your Options?

Short-term health insurance in Texas is a legitimate option for the right situation. Let us help you determine if it fits your needs.

Get Your Free Consultation →Call Wilkerson Insurance Agency at 214-501-9613 or visit wilkersoninsuranceagency.com to compare your options. You can also request a quote online. We are based in Farmers Branch, TX and serve clients across the state.